Cover image: An illustration by John Francis Knott that appeared in the Dallas Morning News, May 24, 1945. The relentless war bond campaign during WW2 was an attempt to reduce the rapidly expanding money supply during wartime spending to stave off the ravages of inflation.

Mike Green noted in a Substack article that when he invited Warren Mosler to meet Peter Thiel, at the end of the conversation, Thiel’s reaction to Mosler’s compelling explanation of his Modern Monetary Theory was that it was probably true, but if the general population found out this is actually how it works, it would break the system. In other words, when people and politicians find out that they can literally vote for more money, it could threaten capitalism as we know it.

I’d argue that, following the 2008 and Covid crises, everyone who was paying attention or gave a damn did find out. They lived through the crisis, saw the massive government spending, and consumed the subsequent deluge of news about a revival of Keynesian-adjacent economic ideas like UBI. But modern information systems are ephemeral and distorted. For many it didn’t compute, faded from memory as conditions improved, seemed like yet another conspiracy theory, or reinforced a broad cynicism about the financial system. Politicians continued parroting the same “debt cliff” talking points while the debt ballooned. Nothing happened. People had lives to live and bills to pay.

But deficits and debt do matter, and Modern Monetary Theory never claimed they didn’t. We’ll belabor the point later, but this is the thesis we want to unpack: if inflation is the true constraint of modern economic theory, how do we navigate the greatest supply disruption of petroleum in history?

Over the past week, I watched a few old in-depth PBS documentaries about the presidencies of Herbert Hoover and Franklin Roosevelt. It was interesting to look back a century at Hoover’s term — a man whose legacy is usually summed up as the president who did too little too late to prevent the Great Depression, and even exacerbated it with miscalculated policies like tariffs and a sharp reduction in government spending. But when Hoover was president, the Federal Reserve was still a bumbling institution of stodgy old men and the idea of direct government intervention into free enterprise was sacrilege. The federal government had only just begun to create regulatory frameworks for banks, businesses and markets. Economists of the era were still using the constructs of the 19th century. John Maynard Keynes was a young man, only beginning to formulate the theories that would revolutionize economic policy. Milton Friedman, who would later resoundingly prove that monetary contraction led to the depression was still a teenager.

When FDR assumed power in the midst of the Great Depression, Keynes’ radical new economic philosophy figured heavily into the new administration’s financial relief plan: The New Deal. FDR’s subsequent alphabet soup of programs helped the average family avoid homelessness and starvation, but those various make-work and safety net programs only stemmed the bleeding, and it wasn’t until Roosevelt’s third term that the total mobilization of the US workforce toward a wartime economy permanently reversed course and set the stage for the staggering growth for the rest of the 20th century.

Debt spending during wartime was nothing new. In a state of war, governments had always been willing to throw out the rule book and pull all the stops to win. Debt is irrelevant when faced with an existential threat. Keynes’ insight was that wartime economic policy could also smooth out the oscillations of economic contractions, regardless of whether there was a war to be fought. What followed the New Deal and WW2 was essentially a series of US regimes that continuously advocated for spending on “guns and butter” to ensure the economy was booming during the next election cycle.

The wartime economic model of industrial policy didn’t end in 1945 — it continued in the US, its mutations resulted in the economic “miracles” of the tariff and export-driven economies of Germany, Japan, and South Korea. Finally, China and Vietnam adopted it as they pivoted from the Soviet central planning models that failed miserably due to rampant bureaucratic corruption and what amounted to perversely absurd incentive structures and the lack of high fidelity information inherent to market systems. Ask any Chinese citizen walking the futuristic streets of Chongqing if such policies worked, and they’ll probably tell you a story about a parent or relative who was a barefoot rice farmer living in a dirt floor shack thirty years ago.

But the end-game of export-driven economic growth is always the same. Trade is bilateral by definition. A trade surplus is just selling physical goods in exchange for another sovereign’s currency. Export countries grow rapidly by repressing the buying power of workers in their domestic markets, exporting goods and bringing home cash to expand “the physical plant.” The US has historically absorbed most of that export surplus with steep trade deficits. The process reaches a termination phase where the build-out of factories, infrastructure and real estate reaches a limit, creates a bubble, and workers have to be paid more to start consuming in domestic markets, which erodes their competitiveness. That happened in Japan, Germany, Korea and now China, which faces a massive collapsing real estate bubble and a new generation of workers that are ready to level up their standard of living or drop out of the fiercely competitive urban centers, move back to the hinterland with their families and “lie flat”.

Looking back on what works and what doesn’t, it’s abundantly clear that modern economics is still post-Keynesian, and we’re left with minor quibbling between think tanks like Brookings and the American Enterprise Institute on the fine points of how, when and where we should goose the economic machine. One side advocates for monetary expansion and industrial policy with spending and taxation, the other with spending and tax cuts. The emergent compromise is debt, growth, debt, growth ad infinitum.

The post-Keynesian perspective of Modern Monetary Theory takes it a step further with the idea that sovereign debt in a fiat system is relatively real. This is nothing new — German economist Georg Friedrich Knapp proposed the same idea as early as 1905. Rather than try to elucidate an ideal of how it’s supposed to work in a “fair free market,” MMT just describes how the global monetary system actually operates. Sovereign deficits don’t matter until there is inflation, and inflation is usually transitory, uncomfortable and manageable if the sovereign takes the responsible actions at the right times. The national debt doesn’t matter until the cost of servicing it becomes too expensive, and then the sovereign has the option to tax, inflate or print money to buy back debt instruments and hold them on the treasury balance sheet as an asset. Again, regardless of how one thinks it should work, that’s an accurate description of modern monetary operations, not some radical prescription for a funny money system. This continues to drive classical economists nuts, as if it violates a solemn vow to never speak of the shibboleth.

Our economic system is not the mythical creature we call “free-market capitalism” that was fabled to wander the frontier amidst wildcat banks in the 19th century, where every fifteen years a great dragon would appear and wreak havoc upon the villagers with bank failures, mass unemployment and famine. It has evolved into a lightspeed interconnected corporate financial enterprise system serviced by the sovereign central banks and sovereign treasuries of the world. In that regard, the economic differences between so-called Neoliberalism and “Socialism with Chinese Characteristics” have blurred to the point where they may be semantic. To an alien, they would look practically indistinguishable. Both systems are global, stimulate via industrial policy and fiat issuance, encourage fierce competition and creative destruction, balance the profit motive with redistribution and extensively intervene when systemic problems arise.

The “secret” of MMT needn’t be revealed. Politicians and the public were intuitively aware that the spigot had always been on — at least since Reaganomics. Regardless of party, the government spends more than it taxes, while both sides participate in an elaborate theater of great offense that the other side lacks fiscal discipline, which appeals to the sensibilities of households balancing their fragile zero-sum checkbooks. Otherwise, the government would be unable to justify taxation at all if they openly admitted that it actually wasn’t a zero-sum game. Today it is manifest in the cognitive dissonance of populist politics.

American voters, business owners and investors have been conditioned by decades of intervention to expect it, and they navigate risk with that backstop in mind. Things can get bad, but in a worse-case scenario, Uncle Sam will step in and make everyone whole again.

But again, deficits and debt absolutely do matter, because the value of money must remain stable enough to conduct global financial operations and avoid calamitous economic destruction. Beyond that, it’s just an insanely complex game of stock and flow to direct enough attention, energy and matter extracted from the earth or the sun toward productive activity so that everyone can share in the unprecedented abundance of modernity. Inequality and the profit motive are unquestionably effective in holding the system together, but there’s absolutely no reason why anyone should want for basic necessities in the 21st century.

While the dominant arc of post-Keynesian economic policy long prioritized aggressive demand management and government-steered market interventions to stabilize growth, the current administration’s policies, inspired by Stephen Miran have steered the US in a new direction. Miran’s model shifts from federal demand-stimulus programs, advocating instead for sweeping deregulation, permanent tax cuts to incentivize domestic manufacturing, and a targeted use of tariffs to restructure global trade. Unlike traditional post-Keynesian policy, which champion globalism, a highly independent Federal Reserve, and a large regulatory footprint for financial institutions, Miran’s prescriptions seek to actively constrain the central bank’s mandate, accelerate interest rate cuts by factoring in immigration and supply-side efficiencies, and utilize protectionist trade measures as a strategic lever for domestic renewal.

It’s a novel adaptation of the same supply-side policy playbook that conservatives and emerging economies have used for years, and will no doubt be carried on by whatever US administration inherits it, as the tenor of American politics becomes increasingly populist.

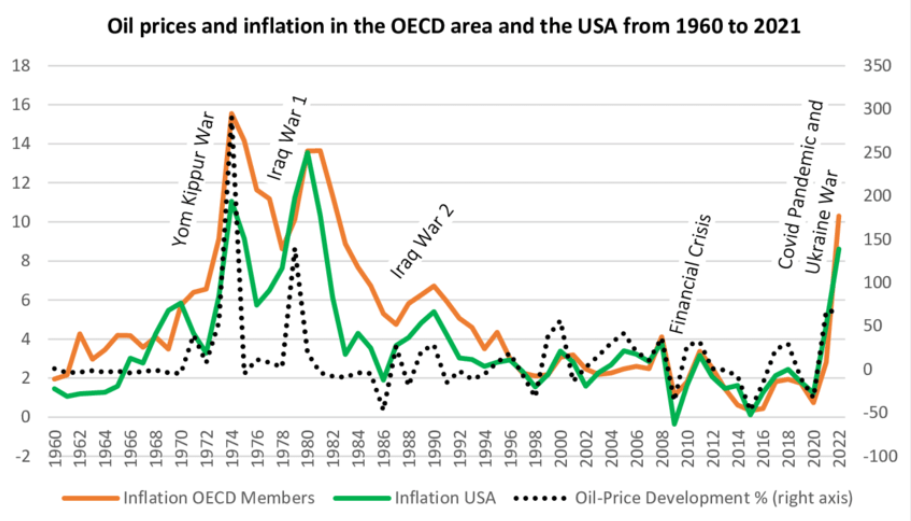

Miran’s framework will be tested by the forthcoming interruption in the petrochemical supply. To be clear, this is the largest petroleum supply disruption in modern history. Miran and his proponents argue an energy shock creates immediate, transitory price spikes in headline inflation, but they are front-loaded and dissipate twelve to eighteen months out. The lag of Federal Reserve moves is too long to curb an immediate supply disruption, meaning the central bank should maintain a steady course toward rate cuts. A sudden spike in oil prices functions as a double-edged sword, acting not just as an inflationary supply shock, but simultaneously as a powerful negative demand shock. As consumers are forced to divert larger portions of their disposable income away from general goods and services just to cover higher gasoline and necessary needs, a natural process of demand destruction takes hold across the broader economy.

A plausible consequence of this dynamic, especially when aligned with a cooling and shrinking labor market, is that the deeply disinflationary forces of demand destruction would quickly neutralize or even overwhelm the initial inflationary surge. For a policymaker adhering to Miran’s viewpoint, this structural softening means forward-looking inflation expectations remain anchored, rendering an aggressive hawkish monetary response counterproductive. Instead, the combination of organic demand destruction and aggressive supply-side deregulation is expected to steadily pull inflation back toward target levels within a year, allowing the central bank to “look through” the temporary energy spike and focus on preventing an asymmetric rise in unemployment.

I have to agree with Miran’s thesis. It’s precarious. Historically, the correlation between major energy shocks and economic downturns is exceptionally strong, with roughly eighty percent of all global and US recessions since World War II being preceded by a significant spike in oil prices. The worst case is a protracted stagflation, but the K-shaped economy makes that less likely if credit conditions remain favorable for consumers and businesses.

It is likely the Federal Reserve will realize the futility of rate increases, and a stalemate will lead to no changes in the overnight fed funds rate in 2026. It’s hard to understate the potential impact of this historic supply shock, which should not be taken lightly. The consensus among economists assigns a roughly 50% chance of recession as a result.

Meanwhile, investors are left with few clear options. All asset classes are richly priced. Fixed income faces interest rate risk. Holding short duration liquid assets like cash and treasury bills faces both inflation risk and the opportunity cost of unpredictable and rapid market rebounds. The relatively nominal P/E ratios of the market are challenging to decipher. It’s not the P, it’s the E that concerns analysts. The forward earnings of AI stocks are extravagant relative to global GDP. They imply aggressive margin growth, extraordinary productivity gains and losers in the rest of the market.

In a January 2026 study by Servaas Storm in the International Journal of Political Economy, surveys of major financial asset managers show that over 50 percent of fund managers explicitly characterize AI stocks as being in a bubble, while a net 20 percent state that corporations are spending too much on data center infrastructure. Concerns regarding massive data center debt have already caused five-year credit default swap spreads to surge for key infrastructure providers, signaling that the credit markets are pricing in heightened default risks associated with the buildout. Lest we forget that markets have been caught optimistically oblivious and flat footed repeatedly throughout history: on July 1914, September 1929, December 1972, August 2000, October 2007, February 2020 etc. If we were looking for an exogenous event to pop this bubble entering 2026, we couldn’t offer a cleaner economic example with historical precedent.

Thus, back to our question of how and why one should continue to participate in the equity and debt markets. The system, no matter how abstract, is far too large to ever cease to yield over time, because it is impossible for the global financial system to stop “expanding and contracting” without ceasing to direct energy toward productive endeavor, which would amount to destroying itself. And there’s nothing wrong with circular reasoning if it’s a tautological description of how financial systems operate.

The Bayesian explanation I’ve personally settled on is that the apparatus of the market is optimized to attract as much capital as possible to the people and businesses who will do something productive and profitable with it, and with governments and private institutions constantly expanding the monetary supply, asset prices go up, regardless of whether it ends up being allocated to productive endeavors that are in the best interest of most people most of the time. As I put it in a previous post, “your magic money number go up because all magic money number go up.” The result is a feedback loop that leads to a concentration of wealth. The rich get richer because their money managers have to buy assets that either grow or preserve wealth against the ravages of inflation, which is a virtuous or vicious circle. In terms of where that money flows, there are worse options than the equities and debt of productive enterprises, but there exists a point where too much capital leads to bad allocation decisions and diminishing returns.

The perennial claim that indexing the market is an unfair, free-rider dilemma that distorts markets may be true (I believe it is), but it doesn’t change the fact that Bill Sharpe’s “five bips cheat code” works damn well long term on a risk-adjusted basis. Passively owning the global market in a well diversified portfolio remains a reasonable core approach to harvesting the returns of the capital apparatus without getting sucked into the psychological traps of the system.

When there’s nowhere to hide, sit back and enjoy the ride.